18th March 2026

Retirement

Maximise your tax benefits with S-Pension starting in 2026!

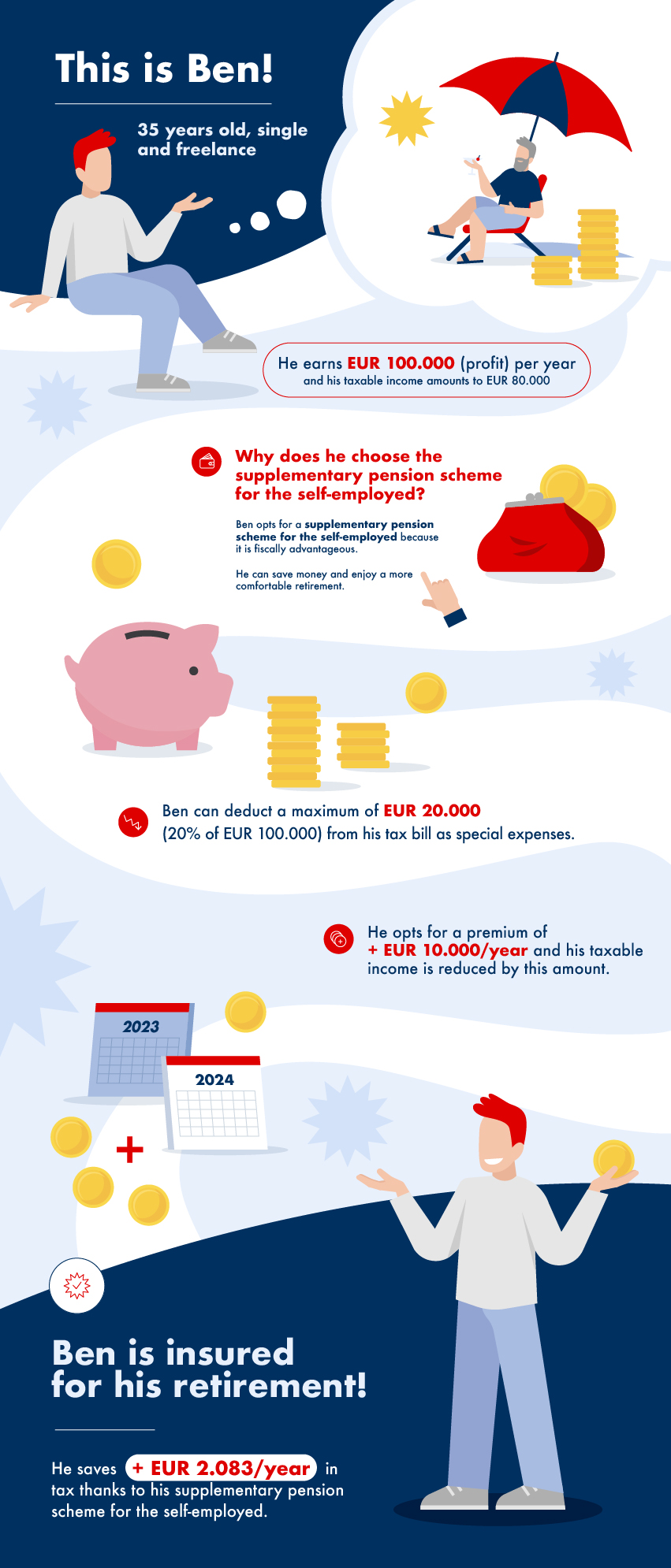

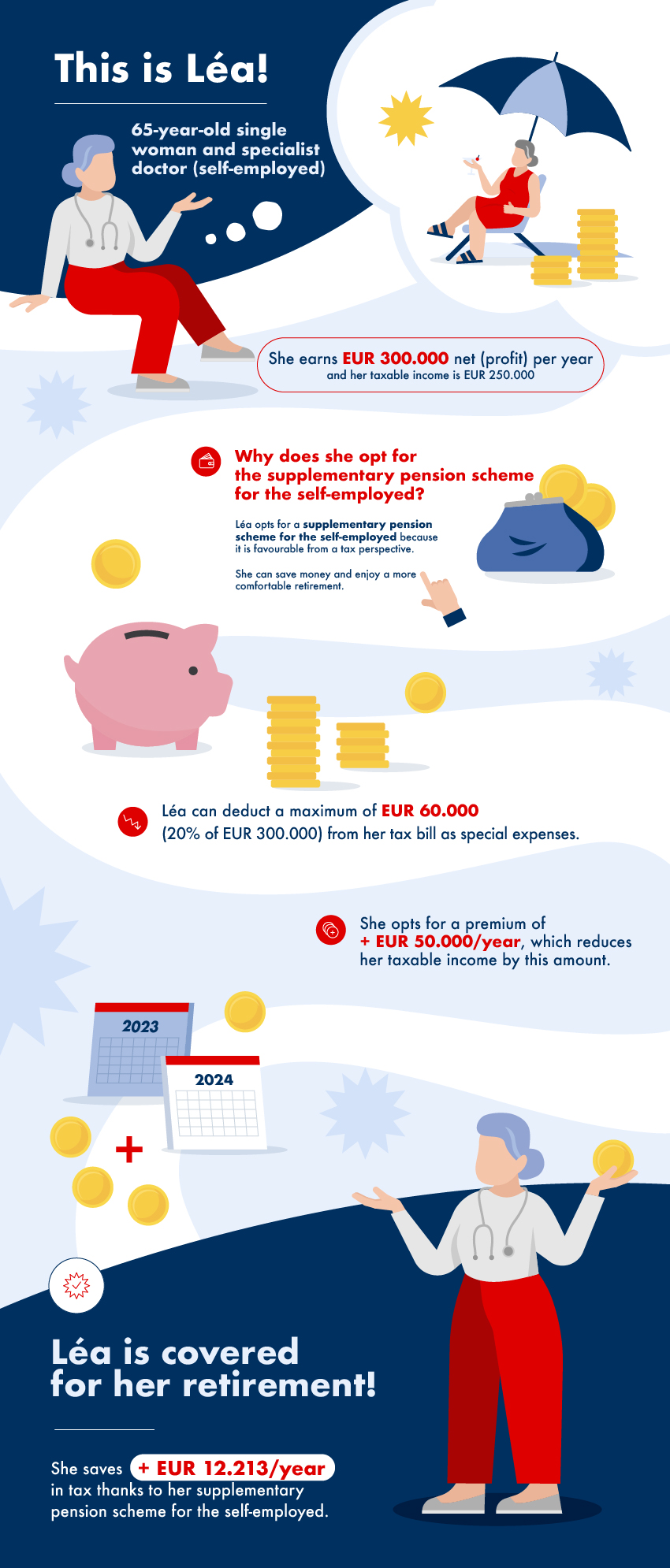

Why Sophie should start her retirement planning today: The workday is over. Sophie is sitting in her living room, laptop closed, tasks completed. Her daughter Lily is already asleep and her husband Marc is at basketball practice. For the first time in a long while, Sophie can enjoy a moment just for herself. She picks up her smartphone and scrolls through the news. Suddenly, a headline catches her eye: “In 2026, contribute more to your retirement plan and enjoy tax benefits in 2027!” Sophie frowns. What does that mean for me? She has often thought about securing her future but kept postponing the decision. One thing is clear: when she retires, Sophie wants a life free of stress and full of comfort.

![[Translate to English:]](/fileadmin/_processed_/4/9/csm_443_Marc_et_Sophie_S-Pension_8eb784f1c7.jpg "[Translate to English:]")

![[Translate to English:]](/fileadmin/_processed_/e/6/csm_399_S_M_Luxtrust_3711851251.jpg "[Translate to English:]")

![[Translate to English:]](/fileadmin/_processed_/9/8/csm_384_S_M_Google_Pay_eba9cd7de2.jpg "[Translate to English:]")

![[Translate to English:]](/fileadmin/_processed_/6/d/csm_360__S_M__Operations_bancaires_simplifiees__LuxTrustMobile_4723518e90.jpg "[Translate to English:]")

![[Translate to English:]](/fileadmin/_processed_/8/6/csm_342__Rentree_scolaire__jeune_avec_smartphone_et_app_bancaires_096fab7fb6.jpg "[Translate to English:]")

![[Translate to English:]](/fileadmin/_processed_/a/0/csm_visa-miles-and-more-340_b8c94aa7bd.jpg "[Translate to English:]")

![[Translate to English:]](/fileadmin/_processed_/f/6/csm_320__S_M__Quand_un_reve_devient_enfin_realite_4ed9dff8d2.jpg "[Translate to English:]")